The rent vs buy debate

Renting is not throwing away money and buying a home is not always a sound financial decision.

The rent vs buy debate is a touchy subject for many. Buying is often seen as an achievement and renting is often viewed as a waste of money. This perception is wrong but persists partially because it’s difficult to compare the true cost of renting to buying. When you buy a home with a mortgage, some portion of the mortgage payment goes to increase your net worth because it pays down the principal of the mortgage debt. People often make the mistake of comparing the mortgage payment to the cost of rent in their city or town and decide what to do based on which one is cheaper. In this article I’m going to talk about how to compare these choices. Note, this is not financial advice.

To request a topic anonymously, fill out this form.

Key points:

You cannot simply compare the mortgage payment to rental payments. Part of your mortgage payment increases your net worth by paying down the mortgage debt, but none of the rent payment increases your net worth.

All homeowners pay rent because of opportunity costs. This is a real economic cost, and any costs above the cost to rent just increases your exposure to residential real estate.

Copy this spreadsheet from Google Sheets to compare the costs for your own situation.

The 5% rule

I think the best framework to approach this problem through is the 5% rule, made popular by Ben Felix. It compares the unrecoverable costs of renting vs buying. The word unrecoverable just distinguishes between the money that pays down the mortgage which increases your net worth and the money that goes to pay your mortgage interest, which is lost to you. Rent, for example, is entirely unrecoverable, but so are property taxes. Ben estimates that average property taxes are about 1% of the value of the home and an additional 1% goes to maintenance and upkeep of the property. So that’s 2% of your home’s value right there you lose per year in unrecoverable costs.

Next, let’s look at a home as an investment. Counter to what I expected, it looks like the return on real estate outpaces1 the return2 of stocks globally, according to page 15 of this paper which attempts to calculate the rate of return of everything. It claims that residential (as opposed to commercial) real estate has been the best performing asset class throughout modern history, primarily due to the volatility for this asset class being lower than stocks and bonds3. In this case, we will use 4.64%4 per year for equities and 6.61% per year for residential real estate. This means that we would actually earn an additional 1.97% by investing in a home over stocks.

Next, we need to address the interest rate on your mortgage. For the sake of this example, let’s just say that your mortgage interest rate is 5%. Assume the downpayment is 20% and the rest is financed with a mortgage, your overall cost of financing the home is 3.61%56. So now, we have 1% for taxes, 1% for maintenance, and 3.61% for the financing costs of the home bringing us to a total unrecoverable cost of 5.61%7 of the value of your home per year. This cost is effectively equivalent to rent.

Now we have everything we need to make a true rent vs buy comparison. We take the value of your home, let’s say it’s $500,000, and multiply $500,000 by 5.61% to get us $28,050 per year in unrecoverable cost, and then divide that by 12 to get the monthly equivalent rent of $2,337. The power of this is that if you can afford to live in your area with the same amenities and lifestyle provided to you by a house that costs $500,000 for less than $2,337 in rent, you should rent, otherwise you should buy. I made a Google Sheet here that you can copy down and experiment with for yourself.

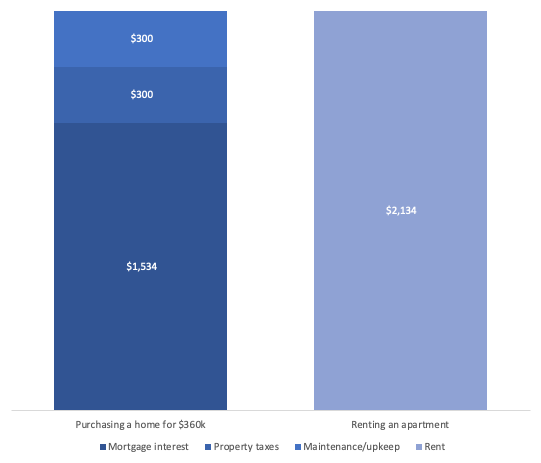

Below is what that looks like on a $360,000 home (which is the purchase equivalent of rent for $2,134). This assumes a 6.39% interest rate on a 30 year mortgage. Please note that I am ignoring the opportunity cost between real estate and stocks because of the contention around if housing actually returns more than stocks do. Some have measured the opportunity cost to be very large in favor of stocks.

Equity

A large part of this analysis hinges on the concept of opportunity cost. This is the cost you experience because of trading off one thing for something else. Another way to think about this is that when you own the home you live in, you are by definition not letting someone rent it out. This means you are trading your housing for their rent. You could be charging someone else rent to live in that property, but since you are not that is a real cost that you are incurring. This means you can decompose living in a purchased home into the rental portion and anything above that is exposure and ownership in real estate. This is a fundamental point, when you own your own home this is financially equivalent to paying rent and owning a real estate investment trust (or REIT), except that in a REIT, risk is spread out across many properties, where your home is exposed to specific risk factors in your community. You should think carefully before purchasing a home and to recognize that there is significant risk in owning a SINGLE home.

One other thing I’ll say too, is that when you own a home, the building loses value, but the land is what actually appreciates over the long term. This means that any buildings on the property lose money over the long term. In other words, there doesn’t seem to be much economic sense to improve and expand a building you own, unless you want to because it will increase your happiness. All this to say that owning a home and renting can be equivalent choices depending on the housing options available in your market.

This in itself a surprising result, as many believe that equities outperform real estate due to the value generating nature of businesses. The low standard deviation (risk) of returns for housing also should imply lower returns, which is a fundamental assumption in financial theory (risk and reward are linked). This assumption is clearly broken when it comes to these housing numbers, so I think they should be taken with a grain of salt.

Both returns are inflation adjusted.

Performance between asset classes must be judged by both the return and the risk associated with it. High returns typically relate to high risk. Risk is typically measured using standard deviation.

We will use the geometric return because this takes into account compounding.

(20% * 1.97%) + (80% * -5%) = -3.61%

Note that as time goes on, these weightings will move toward 100% equity and 0% debt as you pay down your mortgage.

1% + 1% + 3.61%