Smoothing out your costs

Here are some simple strategies to smooth out the costs for things

Previously, I touched on how much to save for retirement. This leaves us with a problem though, and that is how to save for other, non-retirement goals? Imagine you are saving 20% of your income and spending the remaining 80% on monthly expenses. There’s nothing left over to cover larger goals like saving for a downpayment on a house or for a vacation that you’d like to go on. We’re going to talk about how to plan for these goals and a few tools that will make it easier. As a reminder, this article is for informational purposes only, this is not legal, tax, investment, financial, or other advice.

To request a topic anonymously, fill out this form. To reach me with questions, please email alexwarfel@gmail.com.

Key points:

Monthly payments occurring at different dates can be hard to keep track of. If these charges aren’t properly accounted for, you could incur overdraft fees if a charge hits and there is not enough money in the account to cover it.

For all non-retirement future goals, you can use high yield savings accounts or brokerage accounts to save for them.

If you’re saving for something in the future, you don’t need to save the full amount. You can save a consistent, small amount each month and let interest cover the rest.

Here is a framework for thinking about future expenses:

Monthly spending - Spending that has a consistent cost, and is charged the same time each month automatically.

Short and medium term goals - Spending on a single item in more than a month but less than a year OR spending a lump sum every year. Examples include gifts for family members around the holidays, a yearly vacation, or typical annual car maintenance costs.

Long term goals - Expected spending more than five years from now. This could include saving for a vacation home, or an addition to your house.

Monthly spending (consistent charges each month)

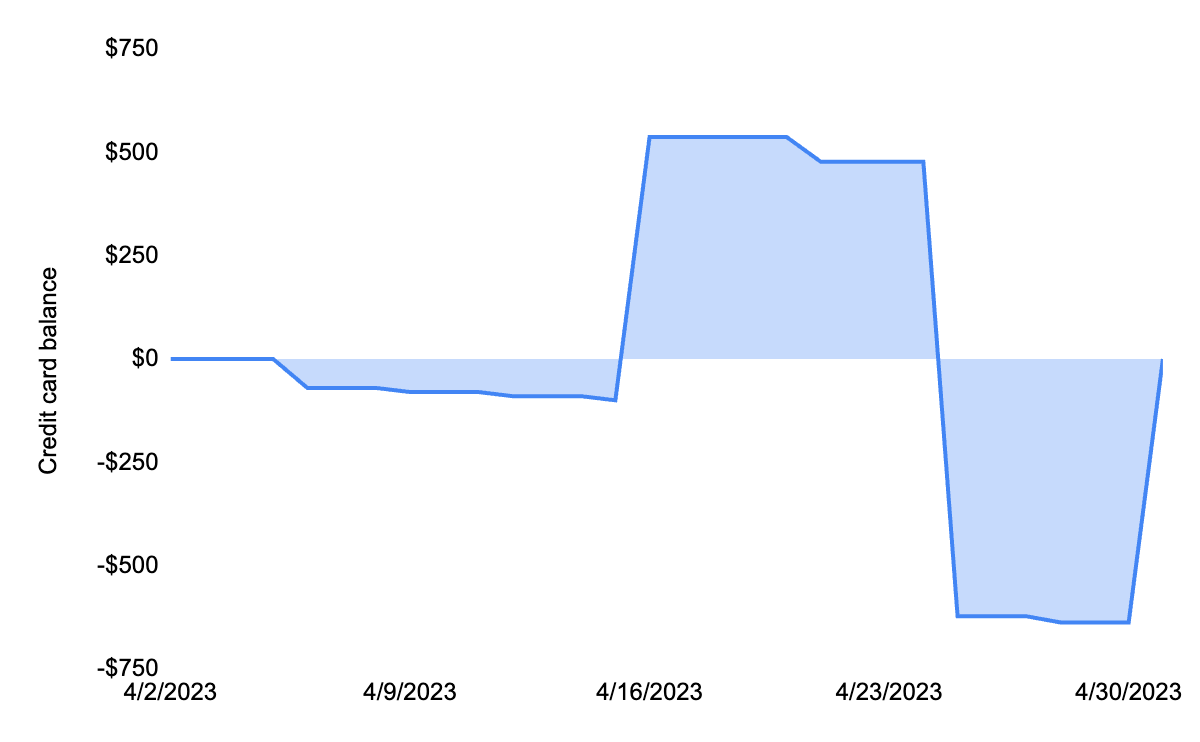

First of, the shortest term spending. Imagine you’re paid twice a month on the 15th and the end of the month. If you actually are, no need to imagine. You get your paycheck and you save a consistent amount but all of a sudden your insurance payment, rent payment, and cell phone bill all come due on the third and fourth of the month. You now have to wait another 10 days until your next paycheck to go out to eat or spend on other things you budget for. The problem here is that people often have random charges for subscriptions or payments throughout the month that don't really align with when they are paid. It looks something like this:

Where the $1,100 charge is rent, and the rest are small charges. Insurance payments, internet bills, etc tend to fall in this category. It would make sense then to total up all of your subscription expenses, put them all on a credit card, and each paycheck put half of those total expenses onto the credit card. This helps you build credit without ever being charged interest and can smooth out monthly commitments leaving anything leftover for regular spending. This also means you can keep your credit card at home so you aren’t tempted to spend on it when you’re out and about.

This is what your credit card balance would look like by smoothing out all of your subscription expenses into just two single payments each month that you pay when you get a paycheck (negative amounts are what you owe).

Remember, you can add money to your credit card balance, and it will just go toward future expenses. Pretend your rent payment comes out on the 24th instead.

Essentially, this just syncs up your monthly commitments with your paycheck to make paying everything more straightforward.

Short and medium term goals (more than a month but less than five years)

For these goals, you can use high yield savings accounts (HYSA) to your advantage. Many providers will let you set up as many HYSAs as you like, meaning you can have an unlimited number of goals. Marcus is great, but there are other options too that you should check out. Let’s consider an annual expense you want to save for, like a $2,500 vacation every year. All you need to do is put $2,500 / number of paychecks per year, in this case 24, into the HYSA labeled for vacations. If you are just starting, you may have to increase your payments because you won’t have a full year until the trip/expense. We’re in May right now, but let's say your trip is in August. Just divide the $2,500 by the number of paychecks until your trip and set that aside. Then, after the trip, reset to saving just $104 (2500/24). This is much more manageable than shelling out the full $2,500 from somewhere else to pay for your trip, or putting it all on a credit card and paying the balance down slowly while getting charged interest.

Now, let's say you’re planning to purchase a car for $15,000 in three and a half years. Let's assume your HYSA currently pays out 4% per year, and the exact number of months comes out to or 42 (about three and a half years worth of months). You would only need to save $14,000 over the course of 42 months because you will make up the extra $1,000 in interest over time. Since this interest rate on your HYSA can change, the amount that you need to save each month or each paycheck could change too. Inflation will also erode your purchasing power, but you can adjust for that by taking the difference between your HYSA rate and the expected inflation rate (you can probably get away with just using the 10 year treasury rate as a proxy for inflation). You can calculate this amount pretty quickly using the PMT function in Google Sheets or Excel.

Long term goals (longer than five years)

These goals are pretty large and are far out in the future, like paying for college for your children or buying a midlife crisis car. These goals warrant investment in a mix of equities and bonds, and you can set up a brokerage account to save for them. You should look into tax advantaged options for your goal too, for example you can open a 529 plan for future education costs.

Conclusion

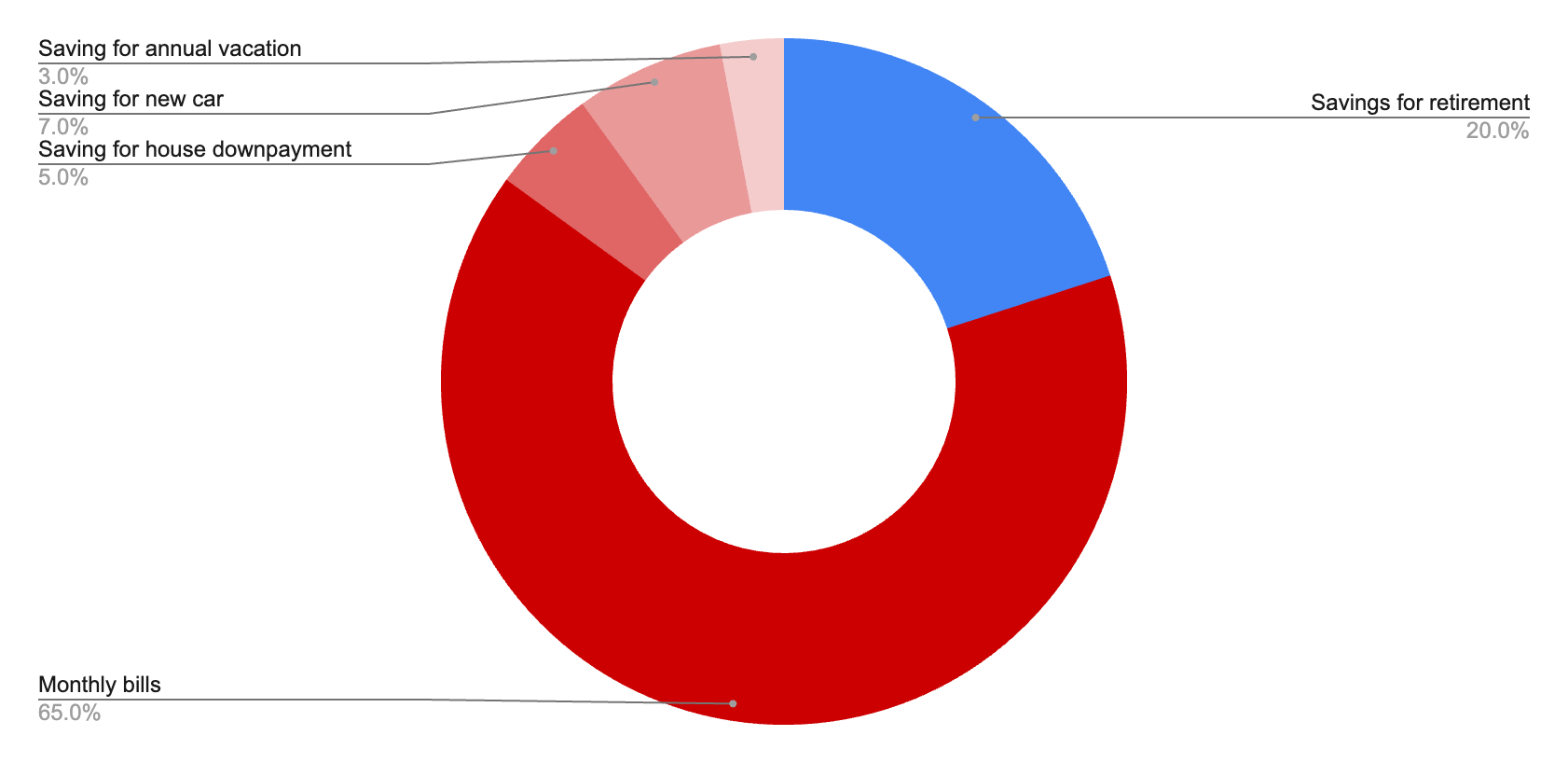

Utilize the tools available to you and you’ll be able to avoid interest payments while also being able to splurge on big expenses. Planning for things will always be a better option than hoping you have enough money in your bank account to do something you want or, alternatively, deciding to not do something because you’re worried about the financial stress it’ll cause. By not thinking through these issues you’ll cost yourself either a ton of money in interest payments or a ton of financial anxiety. Having a system in place to handle these things puts you in great financial shape. Here’s what your cashflow would look like at each paycheck with such a system.

Support

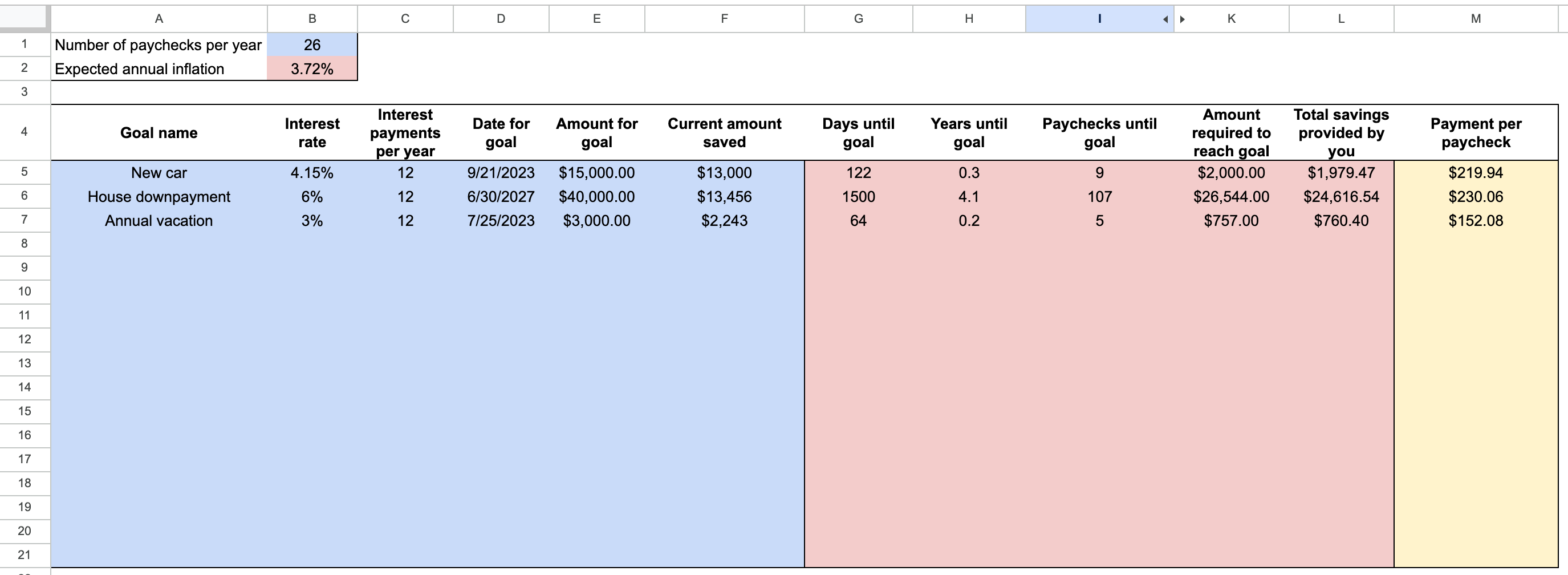

If you’ve enjoyed this article and you’re interested in calculating these numbers for yourself, I’ve put together a spreadsheet letting you add goals to see how much you need to contribute to that goal each paycheck. It’s a template, so you can copy it down and change the assumptions privately. I’ll also reach out with any updates to this template as I make them. Below is an example of what it looks like. See the example below. I appreciate your support!