Your Fund Manager Has to Guess

Why the market requires it, and how to tell good guessing from bad.

In early 2006, Michael Burry sent a letter to his investors explaining why he wouldn’t return their money.[1]

He had spent months reading the actual mortgage loan prospectuses that almost no one else read, the original documents rather than the ratings-agency summaries. He concluded that the subprime mortgage market was priced as though catastrophic defaults were nearly impossible, and the securities built on top of it were fundamentally mispriced. He had built a position in credit default swaps, instruments that paid out when mortgage pools failed. The trade was costing him money in premiums every month. His investors, watching returns lag while markets hummed along, filed to redeem.

He refused to return their capital and imposed restrictions on withdrawals.

When the subprime market collapsed and credit markets seized, Scion Capital’s housing bets paid out substantially while the broader market fell sharply.[1:1] The investors who had tried to leave, had they been permitted to exit, would have missed the payoff entirely.

The Burry case gets cited as a story about conviction. It is also a story about what fund management actually requires. Not just being analytically right. Maintaining a correct thesis, at real professional and personal cost, through the extended period when the market hasn’t agreed yet. That is a different skill. Understanding why they’re different tells you most of what you need to know about how to evaluate a fund manager, or pressure-test your own portfolio decisions.

The market requires uncertainty

Capital markets function, in part, because no single participant can reliably predict outcomes. This is more than an empirical observation about how hard it is to beat the market. As a structural matter, the logic runs like this.

If a manager could systematically generate persistent alpha (excess returns above what factor exposures and market risk would predict), the rational move would be to keep concentrating capital into the strategy until their position size moved prices rather than discovered them. At that scale, they’re no longer finding value. They’re setting it. The market’s price discovery function (the mechanism that connects stock prices to real economic information) collapses.

Consider the alternative version. If the edge depended on information others didn’t have, at scale it starts resembling insider trading. The legitimacy of capital markets depends on genuine uncertainty being preserved.

This isn’t an argument that active management is useless. It is a constraint on what active management can honestly claim. A manager who tells you they’ve found a systematic edge generating consistent excess returns, year after year, without a compelling explanation for why markets have failed to compete it away, is most likely describing luck or factor exposure in disguise. A manager who says “we have a process for being wrong productively, for surviving the period when the market disagrees, and for knowing when a thesis has actually broken” is describing something that can exist within the system’s actual constraints.

The distinction matters because the first kind is common and often markets well. The second is rarer and harder to evaluate from a factsheet.

Three edges that survive

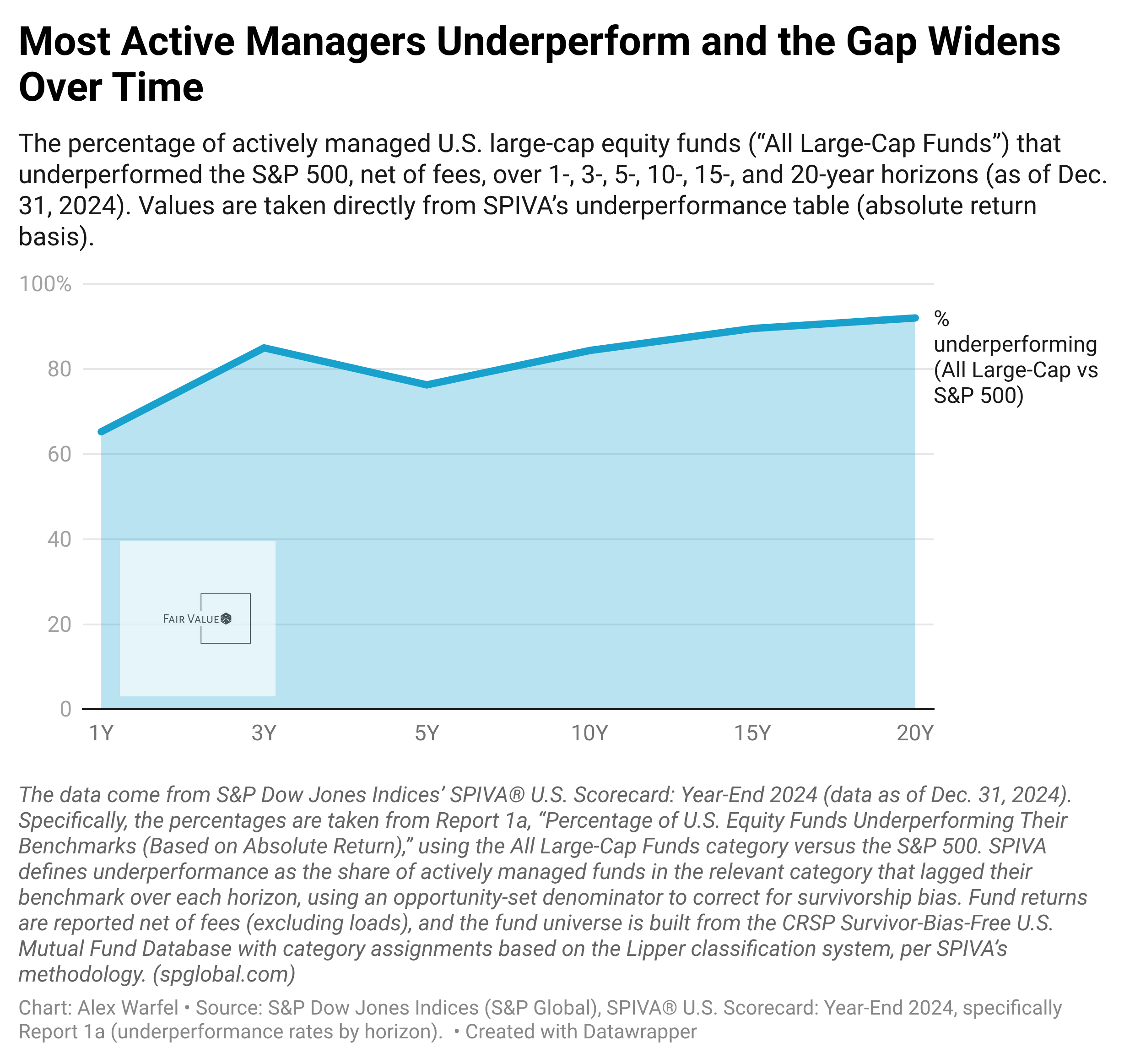

Most of what gets called alpha is factor exposure in disguise. Tilts toward value, momentum, and quality are documented, well-studied risk premia that investors can now access cheaply through factor ETFs.[2] Strip out those exposures from a manager’s reported returns, and excess performance often shrinks considerably. S&P Global publishes annual persistence scorecards showing how rarely this year’s top-quartile managers appear in the top quartile five years later.[3]

Three edges survive closer scrutiny.

Persistence means consistency across full market cycles, not hot streaks within a single phase. Short-run persistence (beating a benchmark for two or three consecutive years) is mostly noise. The test that actually discriminates is whether a manager has navigated a recession, because that’s when liquidity dries up, correlations between assets spike, and credit conditions stop following the patterns visible in calm markets.

There’s an age asymmetry here too. Younger managers who’ve never worked through a real downturn may be analytically sharp but missing the pattern recognition that only forms by living through one. Older managers can have the opposite problem, deep pattern libraries built from prior crises that they fail to update as the world changes. The ideal profile is a manager who has seen genuine stress and hasn’t stopped updating their priors. It’s a narrower window than most manager searches treat it as.

Mean reversion compounds the persistence problem. Managers who lead a decade rarely lead the next, partly because the factor tilts that rewarded them in one market regime carry costs in the next. Persistent outperformance, adjusted for factor exposure and for the base rate of luck across a 10-year sample, is a genuinely rare finding.[3:1]

Catalyst discipline is the piece almost every fund evaluation skips, and it’s where the Burry story does its real work. The question isn’t only whether the thesis is correct. It’s what has to happen for the market to agree with the thesis, on roughly what timeline, and what the loss scenario looks like if the catalyst takes longer or never arrives.

Burry’s thesis (that subprime mortgage securities were mispriced) was correct starting in 2005. The catalyst that forced the market to agree, the actual default wave hitting securitized pools at a scale that shattered ratings assumptions, didn’t materialize until 2007. In the gap, his positions were bleeding premium, his investors were filing redemption requests, and he was right with no one agreeing yet. If he’d been forced to sell in 2006, a correct thesis would have produced a loss.

The harder version of this problem is the Kodak corollary. Kodak’s decline was analytically visible for years before the company collapsed.[4] A short thesis held too early didn’t produce a clean exit. The industry shifted in stages, the stock moved in ways that didn’t map neatly to the narrative, and the timing was unforgiving. Correct analysis. No reward. The market moved on.

Process quality is the hardest to assess from outside a fund, and the research signal here is worth knowing about with appropriate caution. Academic work on investment networks has found that fund managers who share educational or board-level connections with company insiders tend to earn higher returns on their connected holdings.[5] The causation is genuinely unclear. Great managers may attract proximity to strong networks rather than gain their edge from that proximity, and there’s a plausible selection story where skill and network centrality are jointly determined. That ambiguity limits how much any individual investor can take from the finding.

The underlying question is more useful than the research. How does a manager gather information? How do they challenge their initial thesis? What specific signals cause them to exit a position they still believe in analytically? A manager who can answer those questions concretely is demonstrating the process discipline that survives losing periods. A manager who points to their conviction as the process has told you something honest, just not something reassuring.

The Alpha Audit

These three edges combine into a three-question framework for evaluating any active manager, or any investment thesis you’re building yourself.

Has this manager been right and been paid for it across a full cycle, including a real downturn? Can they articulate what has to happen for their current thesis to be correct in the market’s eyes, and what would invalidate it? How does their process work specifically when they’re wrong?

Concrete answers to all three suggest the edges that can actually exist within capital market constraints. Confident answers about past returns, a compelling narrative, and some version of “we take a long-term view” suggest something different.

The Buffett reference deserves a direct response, since he comes up in almost every conversation about active management. The 10-year public wager Buffett made against Protégé Partners (wagering that a low-cost S&P 500 index fund would outperform a portfolio of hedge funds over the decade starting January 2008) is correctly cited as evidence that passive beats active. It does support that. But the less-cited detail is that in the early years of the bet, the hedge funds partially cushioned 2008’s losses, and Buffett’s position appeared to be trailing.[6] He maintained the thesis. The catalyst (sustained equity market appreciation over a decade) eventually materialized decisively.

Being correct is a necessary but not sufficient condition for being paid.

What this means for building conviction

The same framework applies when you’re the one making decisions.

Most individual investors who hold individual stocks have a thesis. Far fewer have articulated the specific catalyst that would cause the market to agree with them, or what they would do if that catalyst doesn’t arrive within a reasonable window. The behavioral research on investor trading documents a consistent pattern. People tend to hold losing positions too long, waiting for vindication, and sell winning positions too early, before the thesis has fully played out.[7] The disposition effect, as it’s called in the behavioral finance literature, is partly a catalyst-discipline failure. The investor believes the thesis is correct but has no clear view on timing or the exit condition if the thesis breaks.

The Alpha Audit applied to your own portfolio is just two questions. What has to happen for this thesis to be correct in the market’s eyes? And what’s the exit if that doesn’t materialize in three to five years?

A manager or investor who can answer both concretely is working with the market’s constraints rather than against them. A fund manager who claims to have solved the guessing problem isn’t offering you an edge. They’re offering you a story. Those are different products, and over most measurement periods, the story has been the more expensive one.

The investors who tried to leave Burry’s fund in 2006 almost missed the vindication. The market eventually agreed with the thesis. By then, they’d been locked in for two years, holding a position that had bled premium and patience in equal measure.

The timing was the variable no one could control. Not Burry, and not them.

That’s the job.

This post is general education only and not financial advice. Past fund performance does not predict future results.

Footnotes

Michael Lewis, “Betting on the Blind Side,” Vanity Fair, April 2010. Available at vanityfair.com/news/2010/04/wall-street-excerpt-201004. For Scion Capital’s performance record, see also “Scion Asset Management,” Wikipedia, accessed February 2026.

S&P Dow Jones Indices, “The Story of Factor-Based Investing,” research report. Available at spglobal.com/spdji/en/documents/research/research-the-story-of-factor-based-investing.pdf.

S&P Dow Jones Indices, “U.S. Persistence Scorecard Year-End 2024,” published 2025. Available at spglobal.com/spdji/en/spiva/article/us-persistence-scorecard/.

Chunka Mui, “How Kodak Failed,” Forbes, January 18, 2012. Available at forbes.com/sites/chunkamui/2012/01/18/how-kodak-failed/. The broader point about timing risk in declining-industry shorts is analytic inference from the publicly available Kodak timeline; the specific trading outcome described is illustrative, not drawn from a documented case.

Lauren Cohen, Andrea Frazzini, and Christopher Malloy, “The Small World of Investing: Board Connections and Mutual Fund Returns,” NBER Working Paper 13121, May 2007. Available at nber.org. The paper finds that fund managers earn higher returns on stocks to which they have educational or board-level connections. Whether this reflects information advantage, or the joint determination of skill and network centrality, is contested in the literature.

Warren Buffett, Berkshire Hathaway 2017 Annual Shareholder Letter, released February 24, 2018. Available at berkshirehathaway.com/letters/2017ltr.pdf. Includes a year-by-year table of S&P 500 index fund returns vs. Protégé Partners’ fund-of-funds portfolio, 2008–2017. For the opposing view from Protégé’s side, see Ted Seides, “A new twist on an old bet with Buffett,” Financial Times, July 9, 2025.

Hersh Shefrin and Meir Statman, “The Disposition to Sell Winners Too Early and Ride Losers Too Long,” Journal of Finance 40, no. 3 (July 1985): 777-790. For a large-sample retail investor replication, see Terrance Odean, “Are Investors Reluctant to Realize Their Losses?” Journal of Finance 53, no. 5 (October 1998): 1775-1798.