Humans Need Not Apply?

AI becomes a hiring filter, markets struggle with volatility, and macro forces hint at a new economic order.

Programming Note: This issue was written as of Wednesday, April 9th at 7:30 PM PT. If major developments occur after that—especially around trade policy or tariffs—they aren’t reflected here.

Key Takeaways

In the news: AI is no longer just a productivity tool—it’s becoming a hiring gatekeeper, with companies like Shopify requiring teams to prove a human is necessary before adding headcount.

Chart of the week: The S&P 500’s strongest five-year returns followed modest 3% monthly gains—not major surges or crashes—challenging the idea that market timing is essential.

Beyond bias – Action bias: Investors often act impulsively during volatility, even though frequent trading consistently harms long-term returns.

Building wealth – Time audit: Tracking your time in 30-minute blocks can uncover “hidden hours” that, once reclaimed, become powerful levers for building wealth.

Historical perspective: This week’s tariff pause doesn’t erase the signal—it reinforces it: protectionism is back in the policymaker’s toolkit. History shows that even the threat of tariffs—when coupled with real investment—can catalyze innovation and industrial renewal.

Literature review – Narcissism + gender: A new study finds narcissistic female CEOs significantly outperform their peers, boosting both profitability and valuation more than narcissistic male CEOs.

In the news

Corporate leaders are increasingly embracing AI as both a productivity tool and a headcount filter. At the same time, U.S. financials are seeing selective strength going into earnings season. But beneath these headlines, Ray Dalio warns that the economic system underpinning it all may be undergoing a rare, generational reset.

Zoom in: Shopify’s AI ultimatum

Shopify announced it will no longer approve new hires unless teams prove AI can’t do the job. CEO Tobi Lütke described a new expectation that employees must integrate AI into their workflows, with AI utilization even becoming part of performance reviews.

“I don’t think it’s feasible to opt out of learning the skill of applying AI in your craft,” Lütke said. “You are welcome to try, but… I cannot see this working out today, and definitely not tomorrow.”

Shopify joins a growing list of firms prioritizing AI fluency in hiring and performance evaluation, while broader white-collar hiring slows. AI-related job postings remain robust, particularly for candidates who can deploy models or fine-tune workflows using generative tools.

The big picture: AI is becoming a headcount gatekeeper.

Rather than augmenting staff, companies are increasingly using AI to replace them—especially in engineering, marketing, and administrative roles. This shift helps explain why tech hiring remains muted despite overall productivity gains.

By the numbers (source):

IT hiring is down 27%; product management down 23%.

AI-generated code now accounts for 25% of Google’s output.

Time-to-hire has climbed to 66 days as hiring slows and candidate pools swell.

Meanwhile: Financials earnings show resilience

FactSet expects the Financials sector to post 2.3% earnings growth in Q1, outperforming six other S&P 500 sectors. However, the growth is highly uneven across industries.

The standout: Consumer Finance is expected to grow earnings by 23%, led by Discover Financial’s projected EPS jump from $1.10 to $3.37.

Capital Markets earnings are projected to rise 10%, with all three sub-industries (asset management, investment banking, exchanges) contributing.

Banks are expected to grow 5%, with regional banks outperforming large diversified ones.

Insurance, however, is a drag: earnings in this industry are forecast to fall -15%, especially in reinsurance (-50%) and P&C insurance (-30%).

Why it matters:

If you exclude Insurance, the Financials sector would be on pace for a 6.7% earnings gain—suggesting underlying health masked by high-variance subsectors.

Context: Macro risks loom large

Ray Dalio warns that today’s headlines—AI-driven job losses, financial earnings volatility, and trade policy drama—are symptoms of deeper systemic shifts. In a widely shared LinkedIn post, Dalio writes that the global order is entering a rare phase of breakdown that mirrors past eras of debt overhang, trade realignment, and civil unrest.

“Deglobalization, debt addiction, and trust breakdowns are forcing a reset of the monetary, political, and geopolitical orders,” Dalio argues.

He cautions that the U.S. cannot indefinitely rely on borrowing from geopolitical rivals, nor assume it will remain the center of global capital and trade flows in an era of tariffs and populism.

What to watch:

The S&P 500 Financials sector is projected to grow earnings steadily over the next 12 months, from +3.6% in Q2 to +18.9% by Q1 2026.

Meanwhile, AI adoption is likely to accelerate hiring divergence between AI-native firms and traditional employers.

Even paused tariffs—if seen as credible threats—could influence corporate behavior, spurring precautionary shifts in capital and supply chains.

The bottom line:

AI is reshaping hiring before it reshapes jobs. Financials are holding up, but macro risks are mounting. As Shopify redefines productivity and policymakers toy with tariffs, the bigger story might be this: we’re entering a new economic regime—one where debt, power, and productivity are being renegotiated all at once.

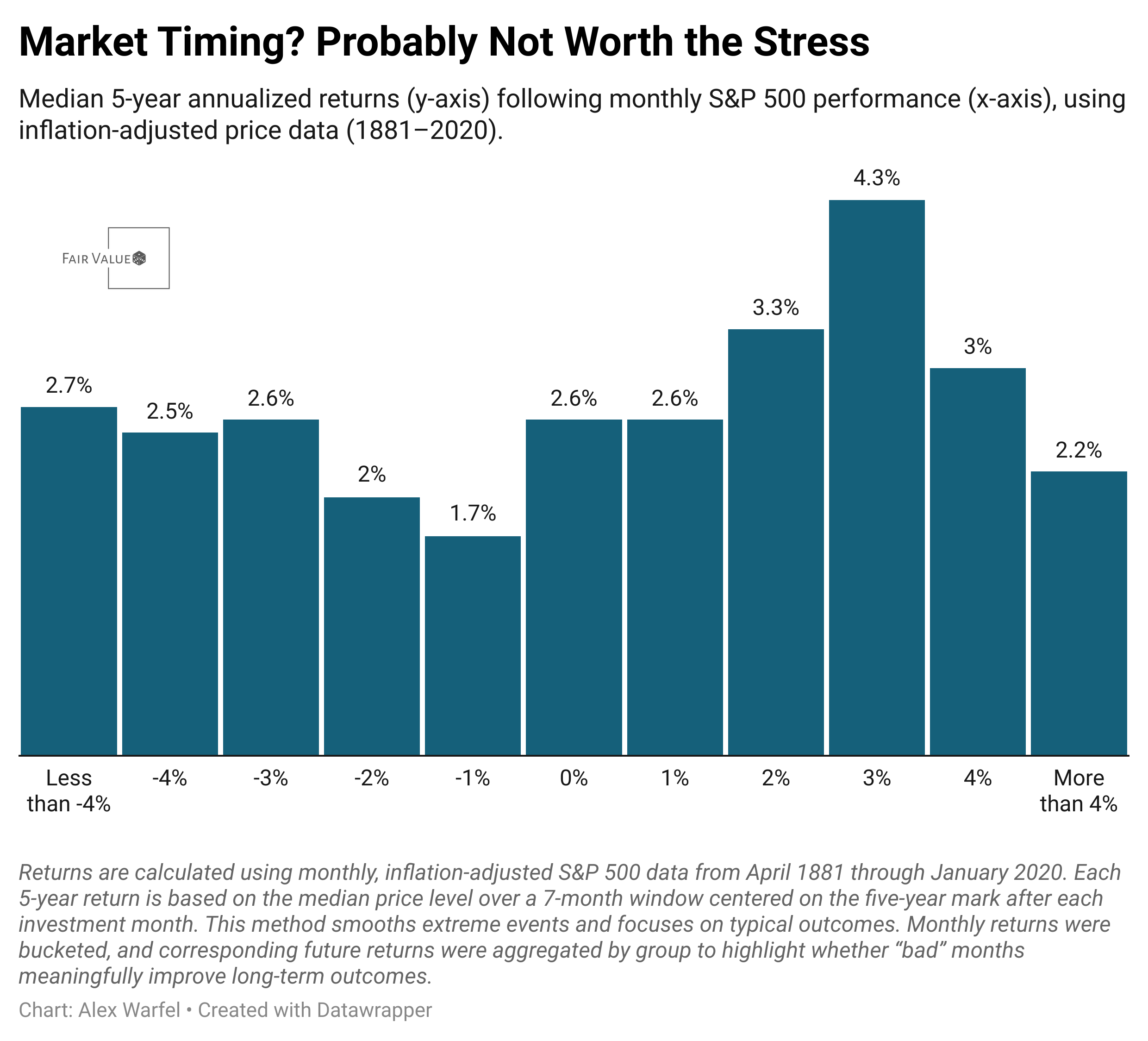

Chart of the Week: The Market Doesn’t Mind a Bad Month

Conventional wisdom says to ‘buy the dip’ and fear down months—but long-term data tells a different story. Across 140+ years of inflation-adjusted S&P 500 returns, the difference in five-year forward performance between extreme monthly upswings and downturns is surprisingly modest. The best future returns came after modest monthly gains—3% months had the highest median five-year return at 4.3%. Meanwhile, sharp monthly losses of more than 4% still led to a respectable 2.7% median return, not far off from the 2.2% that followed monthly gains above 4%. Even the worst-performing bucket (–1% monthly returns) still delivered a 1.7% median annual return—hardly catastrophic, especially when compounded over time.

What this tells us: not only is it okay to have bad months, it’s also okay to miss them. If you didn’t buy the dip this time, you didn’t miss some once-in-a-lifetime opportunity. The long-term path to returns doesn’t depend on catching every bottom—it depends on staying consistent. The market doesn’t punish you nearly as much for being late as it does for being erratic.

Academic research backs this up. Studies by Barberis and Thaler (2003), as well as Dalbar’s annual investor behavior reports, consistently show that investors underperform the markets they invest in—not because the markets aren’t generous, but because behavior erodes results. Emotional responses to short-term volatility, especially fear-driven selling or FOMO-driven buying, are major culprits. In contrast, staying invested through good months and bad—what Vanguard calls the “stay-the-course” strategy—historically outperforms tactical moves based on market timing (Bogle, 2007). Bottom line: if your horizon is 5+ years, the return of the market over the last few days matters far less than your ability to keep showing up.

Beyond Bias: Action Bias — Why We Do Something Even When Doing Nothing Is Better

Action bias is the tendency to prefer doing something over doing nothing—even when inaction would lead to better outcomes. It’s well documented in fields like medicine, sports, and management, where professionals often take unnecessary actions to regain a sense of control or deflect accountability (Bar-Eli et al., 2007). In investing, action bias shows up as portfolio tinkering, panic selling, or jumping into trades to “make up” for past losses—especially during volatile markets. After sharp downturns like March 2020 or spikes like those in late 2023, investors feel compelled to act, even if the best course might be to simply rebalance and wait. This behavior is reinforced by our discomfort with uncertainty and a cultural preference for decisiveness—what psychologist Dan Ariely calls the “illusion of control.” In short: we often trade activity for effectiveness, confusing movement with progress.

Last week’s tariff scare offers a clear example. Markets started to slide on fears of new trade restrictions—but just days later, the administration paused the policy altogether, triggering a relief rally. Investors who acted on the initial fear may have locked in losses and missed the rebound. That kind of whiplash punishes knee-jerk decisions and rewards those who stayed disciplined. To protect yourself from action bias, you need to build friction between impulse and execution. One proven method is using implementation intentions—clear, rule-based plans for how you’ll act during specific market scenarios (Gollwitzer, 1999). For example: “If my portfolio drops 10%, I’ll review my asset allocation, not place a trade.” Research by Barber and Odean (2000) found that frequent traders consistently underperformed less active investors—largely because timing mistakes and overconfidence compound. In volatile markets, the ability to pause, reflect, and not react can be a superpower. Don’t ask “What should I do?”—ask “What will future me thank me for not doing?”

Building Wealth: The ‘Time Audit’ Rule — Reclaiming Hidden Hours for Financial Gain

One of the least discussed but most powerful tools for building wealth is the time audit — a personal inventory of where your hours go each week. Unlike budgeting money, which is more common and intuitive, budgeting time feels abstract. But for most DIY investors, time is the true constraint. It’s the limiting reagent in better research, more thoughtful planning, and higher-earning opportunities. A 2018 study from the Journal of Consumer Research found that people consistently underestimate how much time they spend on low-value activities and overestimate how productive their days are (Tonietto & Malkoc, 2018). That means many aspiring investors think they “don’t have time” to improve their finances — when in fact, they just haven’t looked closely enough. A time audit is how you look.

Start by tracking your time in 30-minute blocks for three days — either with a notebook, a spreadsheet, or a free app like Toggl or RescueTime. Then color-code or categorize the blocks: productive, neutral, wasteful. You’ll likely find “hidden hours” in surprising places — time spent reflexively scrolling, rewatching old shows, or mentally bouncing between tasks. Those recovered blocks can be reallocated: 30 minutes per week reviewing expenses, another 30 setting up automated investments, and maybe an hour for reading or learning about a new asset class. Time audits also help you spot fatigue patterns. If you always crash at 9 PM, don’t schedule financial tasks then — move them to a morning when your energy is higher. This is about kindness, not discipline. Wealth-building is a long game, and reclaiming just 1–2 hours per week for focused effort compounds faster than most people expect. Think of time like capital: audit it, reallocate it, and put it to work.

Add to your Toolbelt

Take control of your financial future with Rainier FM—your AI-powered financial planning companion. FM stands for Financial Model, and that’s exactly what this app delivers: optimized, data-driven financial plans tailored to your goals. Using advanced optimization techniques and AI-driven insights, Rainier FM helps users navigate everything from retirement planning to wealth building with confidence. Pricing reflects the cost of running the service, but I’m actively gathering feedback to refine and improve it. Here’s an example of an insight this app can help you uncover.

If this sounds like something you’d find valuable, feel free to reach out or sign up—I’d love to hear what you think as I continue developing the platform!

Historical Perspective: Protectionism, Innovation, and the Role of American Power

President Trump’s abrupt pause on new tariffs—just hours after they went into effect—was a striking reversal. But the bigger message wasn’t the pause itself. It’s that tariffs are no longer political third rails—they’re back on the table, and markets now need to take them seriously. Even if this round was delayed, the episode reinforced that protectionism is part of the modern policymaking toolkit, not just a relic of the past.

Historically, tariffs often spark panic—and for good reason. They raise prices, disrupt supply chains, and can provoke retaliation. But history offers a more nuanced view. In the 19th and early 20th centuries, the U.S. was one of the most protectionist economies in the world. From the Tariff of 1828 (the infamous “Tariff of Abominations”) to Smoot-Hawley in the 1930s, America repeatedly used trade barriers to shape its economic development. And during much of this period, it became the most dynamic industrial power on the planet. From steel to textiles to telegraphs, American innovation thrived not in spite of tariffs—but arguably because of them.

Why? Constraints accelerate problem-solving. When cheap British goods were shut out, American firms had to build domestic capacity. Economist Ha-Joon Chang describes this as “kicking away the ladder”—a strategy where wealthy nations endorse free trade only after climbing to the top via protectionism. This isn’t just a U.S. story. Postwar Japan and South Korea deployed protectionist industrial policies to nurture globally competitive manufacturing sectors. If today’s tariff threats on semiconductors, EVs, or steel push U.S. firms to automate faster or reshore production, they could spark a similar investment cycle—even if the policies are walked back.

There’s also a national security angle. In previous eras of geopolitical tension, the U.S. didn’t just levy tariffs—it mobilized industrial policy. During WWII, Roosevelt’s War Production Board and the Defense Plant Corporation seeded capacity critical to the war effort. Cold War anxieties drove DARPA funding and semiconductor subsidies that helped birth Silicon Valley. In today’s context—amid fears over China, AI, and rare earth supply chains—tariffs may be less about trade and more about leverage.

Still, tariffs without a productivity push can backfire. The U.S. steel industry in the 1970s offers a cautionary tale: trade barriers without reform only entrenched inefficiencies. But if today’s protectionist signals are paired with smart investments—in automation, upskilling, and advanced manufacturing—they could unlock overdue innovation. Paul Romer’s idea of “constraint-driven creativity” applies here: limiting the easy path (e.g., offshore labor) often pushes firms to build better, more scalable alternatives.

For DIY investors, the key is not whether tariffs are “on” or “off,” but how seriously companies take the threat. Are manufacturers accelerating capital expenditures? Are robotics, supply chain, and energy efficiency firms seeing new demand? Even a paused tariff regime can change corporate behavior. If firms believe tariffs could return—or are simply part of a broader strategic chessboard—they may act now. And that could filter into real, investable tailwinds in select sectors.

Supporting Research

Chang, Ha-Joon. Kicking Away the Ladder: Development Strategy in Historical Perspective. Anthem Press, 2002.

Romer, Paul. “Endogenous Technological Change.” Journal of Political Economy, vol. 98, no. 5, 1990.

Irwin, Douglas A. Clashing Over Commerce: A History of U.S. Trade Policy. University of Chicago Press, 2017.

Atkinson, Robert D. and Stephen J. Ezell. Innovation Economics: The Race for Global Advantage. Yale University Press, 2012.

O’Sullivan, Mary. Contests for Corporate Control: Corporate Governance and Economic Performance in the United States and Germany. Oxford University Press, 2000.

U.S. Congressional Research Service. “Industrial Mobilization During World War II.” RL33688, 2006.

Literature Review: Narcissism, Gender, and Corporate Outperformance — What a Surprising Study Reveals

In a unique and carefully structured study, Aabo and Rønnow (2024) investigate how CEO narcissism interacts with gender to affect corporate performance. Prior literature has shown mixed results on whether narcissistic traits in CEOs are beneficial or harmful for firm outcomes — often leaning toward the negative due to tendencies like entitlement and impulsivity (Grijalva et al., 2015; Ham et al., 2017). But this paper finds a noteworthy exception: when the CEO is a woman, narcissism becomes a performance enhancer. Using a sample of 849 non-financial S&P 1500 firms from 2007 to 2020, the authors find that narcissistic female CEOs outperform their male peers significantly in terms of profitability (ROA) and valuation (Tobin’s Q). A one standard deviation increase in narcissism among female CEOs correlates with a 19% improvement in ROA and a 21.9% boost in firm valuation — an economically meaningful effect.

The paper offers several explanations for this result. First, women tend to score higher in trait agreeableness, which helps moderate the toxic effects of narcissism — such as entitlement or manipulativeness — while still allowing them to benefit from assertiveness, confidence, and charisma (Ackerman et al., 2011; Wille et al., 2018). Second, the “double bind” of female leadership expectations may actually discipline narcissistic tendencies. Because women are socially penalized for dominant or egotistical behavior, female CEOs must carefully calibrate their assertiveness to remain effective — a pressure not always felt by men (Eagly & Karau, 2002). Finally, the authors note evolutionary psychology research suggesting women score higher in empathy, which may biologically buffer the downsides of narcissistic leadership (Christov-Moore et al., 2014).

That said, the study does have limitations. Only 3.4% of CEOs in the sample were women, which raises the possibility that these findings may not generalize as gender representation increases. The authors do attempt to control for this with firm fixed effects and robustness checks, including alternative narcissism proxies and exclusions of crisis periods like 2008–2009 and 2020. Still, the sample size — 76 female CEOs over 13 years — makes the data susceptible to statistical noise. Also worth noting: the study doesn’t claim causality, only association. Though the authors make a plausible argument that narcissistic female CEOs drive performance (rather than being chosen because of it), they acknowledge that further research is needed to confirm this with larger samples or causal instruments.

For investors, the implications are twofold. First, leadership personality traits do matter — but only in context. This study supports the idea that traits like narcissism should not be evaluated in isolation; gender, social norms, and organizational environment all shape how a leader’s traits affect outcomes. Second, in a market increasingly focused on ESG and diversity, this research strengthens the argument that gender diversity isn’t just an optics play — it can have real performance implications. Investors may want to look more closely at leadership dynamics and not just firm fundamentals. More broadly, this paper is a reminder that so-called “negative” traits like narcissism can sometimes be assets when paired with the right moderating forces — a lesson that applies to how we evaluate managers, founders, and even our own decision-making frameworks.

Curious about money, investing, or the economy?

I occasionally answer reader questions in the newsletter—no jargon, just thoughtful, practical insight. If something’s on your mind, tap the button below to send it in anonymously.