Follow the Money, Not the Multiples

In a world where liquidity, demographics, and central banks drive prices, the investor’s edge lies in anticipating the marginal buyer, not obsessing over P/Es.

Equity investors often anchor themselves to the “classics”: dividends, book value, and P/E ratios. These metrics feel concrete, as though buying stock means buying a steady slice of a company’s cash flows. Remember, all financial assets are just contracts. If you think more deeply about the legal contract of stock, it’s really just: a bundle of proxy voting rights and a residual claim on whatever might be left in liquidation. Dividends trickle, book values barely move in a world of intangibles, and P/E ratios expand or contract mostly with liquidity and sentiment. If these anchors are so static, why do prices swing so wildly? The answer lies not in the ownership contract itself, but in the marginal flows of capital that set today’s stock prices.

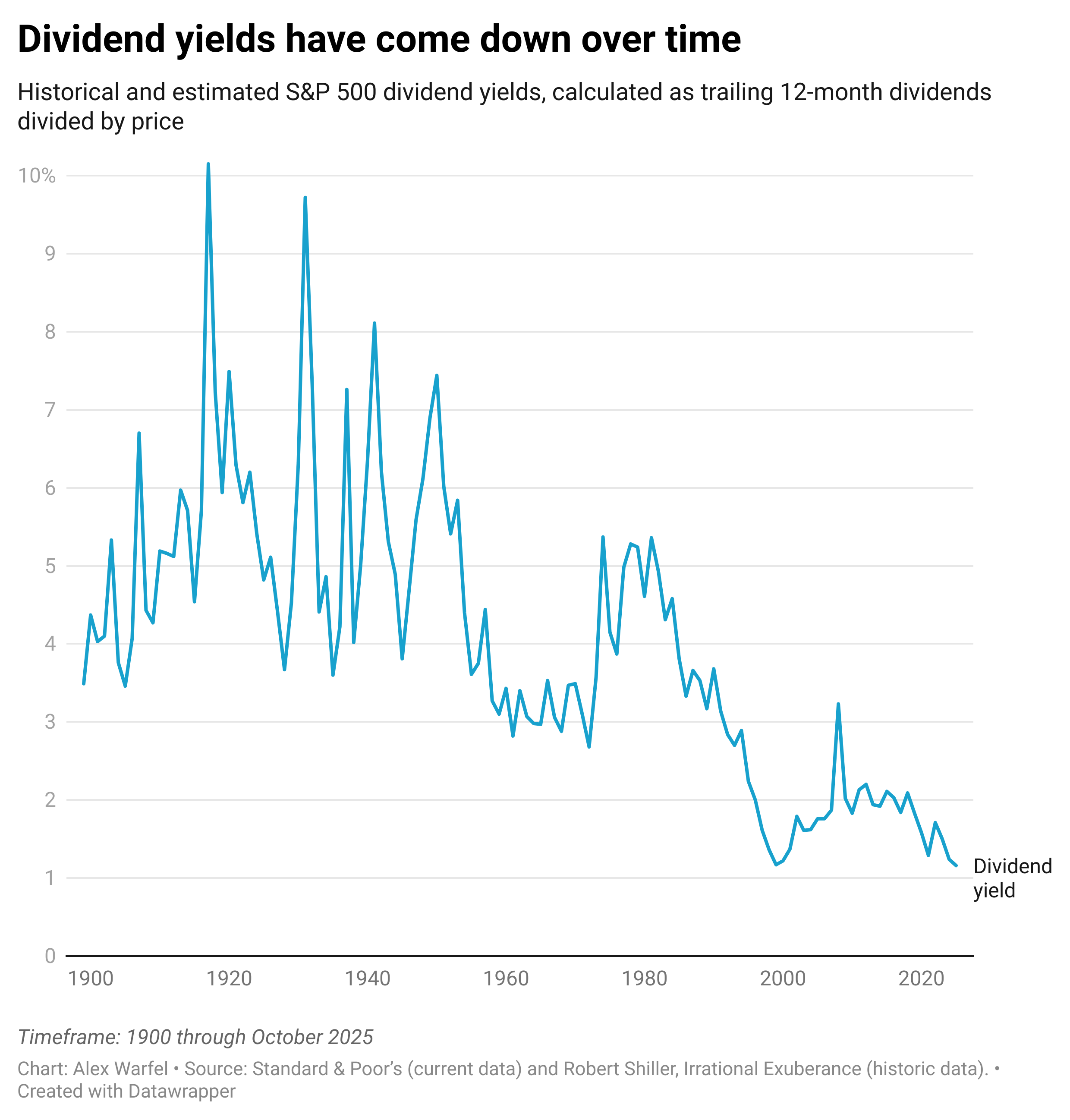

Take dividends, the bedrock of traditional valuation. These have faded as a guidepost. In the U.S., dividend yields have trended downward for nearly a century, falling from 5–6% in the early 20th century to under 2% today (Robert Shiller, Irrational Exuberance).

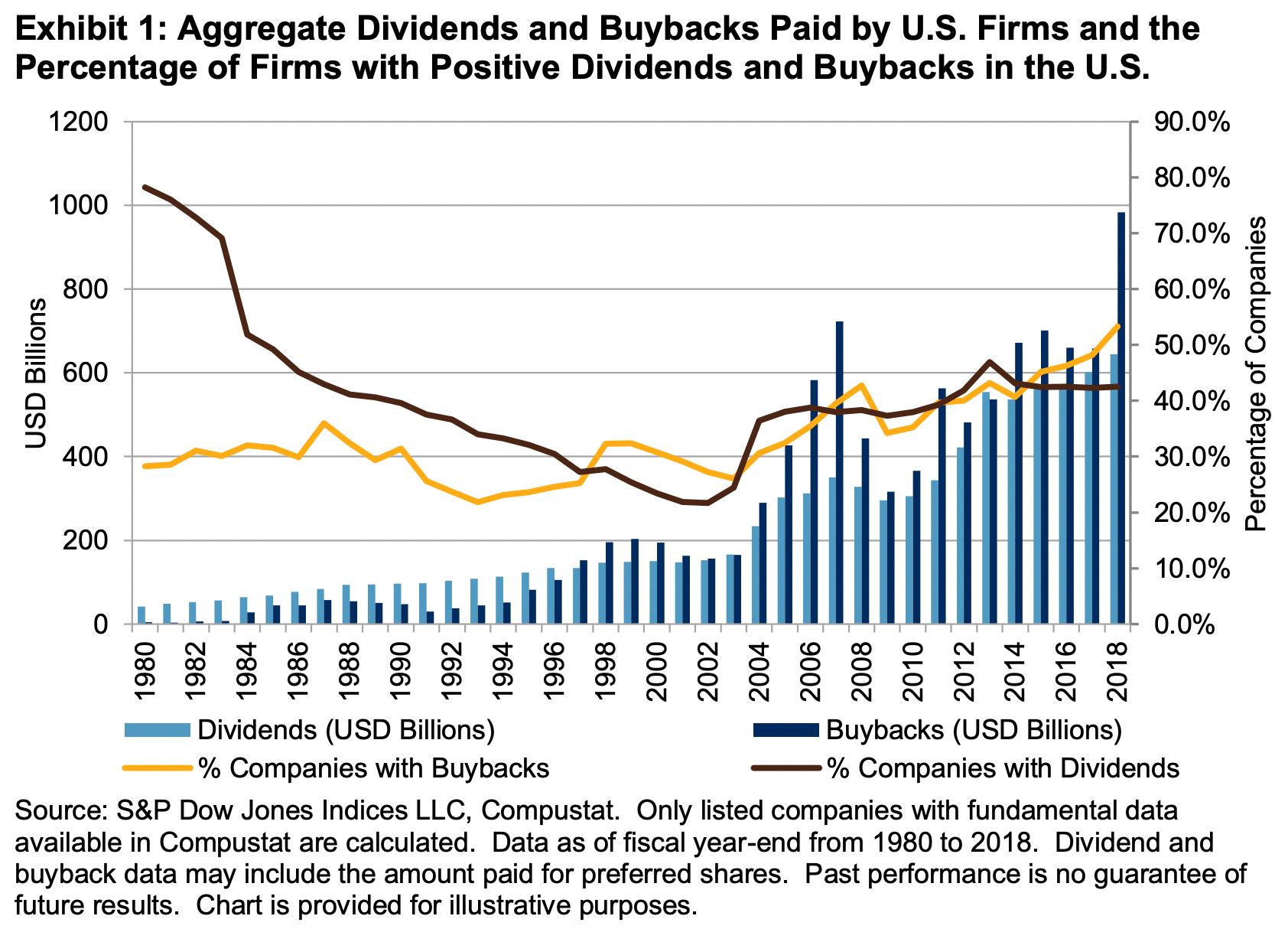

That drop isn’t about taxes; since 2003, qualified dividends and long-term capital gains have been taxed at roughly the same favorable rates. The deeper reason is corporate behavior: companies increasingly favor share repurchases over cash dividends. Buybacks are more flexible, often more tax-efficient, and allow management to support share prices without committing to a permanent payout. Also, cutting a dividend signals to investors weakness in the company, while a buyback is perceived as a one time event (executed over the course of months or years). In fact, S&P data shows that in many years since 2010, buybacks have outstripped dividends as the dominant form of cash return to shareholders.

Book value fares even worse in today’s economy, where intangible assets dominate the balance sheet of the largest companies. Intangibles now account for ~90% of S&P 500 market value. Google’s search algorithm or Coca-Cola’s brand equity don’t show up in “tangible book value,” yet they’re the true drivers of value for those companies. And P/E ratios? They reveal more about liquidity and sentiment than business fundamentals, expanding when capital is abundant and contracting when it dries up. These anchors may offer comfort, but they rarely explain the real, mechanical, force moving prices.

At its core, every asset’s price is set at the margin, by what the next buyer is willing and able to pay. Each bid and ask reflects not a company’s fundamentals, but the momentary balance between buyers with cash to deploy and sellers needing liquidity. That’s why marginal flows matter so much. Demographics channel retirement savings into equities, central banks add or withdraw liquidity through QE and QT, ETFs pull in capital automatically, and global investors seek safety in Treasurys. Even corporate buybacks act as powerful marginal buyers, supporting prices when other flows weaken. To see where markets are headed, don’t ask what an asset is “worth”, ask who holds the next dollar, and where it’s going next.

This lens matters because it explains some of the market’s most puzzling moves in recent years. The 2020–2021 tech rally, for instance, wasn’t driven by a sudden surge in corporate profits, it was fueled by a wall of liquidity, stimulus checks, and zero rates pushing marginal dollars into growth stocks. Crypto’s booms and busts follow the same script: prices surge when new buyers flood in and could collapse when those flows dry up. Even U.S. Treasurys, once the ultimate safe haven, have shown cracks in this framework. In several recent crises, they failed to rally because global marginal buyers, especially foreign central banks, are no longer stepping in with the same conviction. Foreign official investors’ share of total foreign Treasury holdings fell from 59% to 47% in recent years, with private investors now the larger foreign holder base. What looks irrational through the lens of fundamentals often makes perfect sense when you follow the money and ask where the marginal dollar is going next.

Investors should also ask where the past marginal dollars have come from too, and whether those buyers will quickly turn into sellers when conditions turn. Some capital is fickle and quick to exit, while other flows are effectively permanent. In Bitcoin, for instance, millions of coins are locked away forever due to lost private keys, creating a built-in floor of unsellable supply. Analysts estimate that between 2.3 million and 3.7 million bitcoins, or ≈ 11–18% of the total 21 million supply, have been permanently lost (e.g. due to lost private keys), tightening effective liquidity in the market. In equities, the same logic applies: only the most recent trades determine the current price. Tesla’s valuation, for example, reflects the sentiment of the latest buyers and sellers, not every shareholder. Average daily volume (ADV) measures how much of a stock changes hands each day; when ADV is small relative to total shares outstanding, prices are being set by a narrow slice of investors, and that concentration can make markets more fragile.

Stock prices don’t rise because companies “deserve” it, they rise when marginal buyers keep paying more. Valuation ratios assume capital is unlimited, but prices only move when new investors step in. Mispricings don’t correct themselves without fresh demand. That’s one reason why U.S. valuations stay elevated: the country has deep, steady domestic capital. U.S. household exposure to equities has reached record levels in 2025, reflecting a deep domestic buyer base. The true driver is capital at the margin. Over the next decade, the key question isn’t which companies look best on paper, it’s where global capital will feel safest and most productive. Nations with strong legal systems and enforceable property rights will keep attracting those flows. The edge goes to investors who position early, ahead of where the next marginal dollar must go.